Speech by E. Moulin: “Strengthening European sovereignty : from integration to competitiveness”

Authors

Emmanuel Moulin Governor of the Banque de France

Emmanuel Moulin Governor of the Banque de France

Speech by Emmanuel Moulin, Governor of the Banque de France, at the Jacques Delors Conference 2026.

Ladies and gentlemen,

I am delighted to address you on the occasion of the Jacques Delors Conference, held in the auditorium that bears hisname. Allow me to recall its symbolic significance : Jacques Delors began his career at the Banque de France, where he spent the first eighteen years of his career, before going on to become a distinguished Minister for the Economy and Finance and a leading figure in the construction of the European Union. The theme of this conference, moreover, echoes his legacy : “The European Union’s ambitions tested by its resources”. These ambitions are now clearly defined: we must strengthen European competitiveness and boost sustainable growth, enhance strategic autonomy in monetary, technological and defence matters, and successfully achieve the green transition. But these objectives require resources. As Mario Draghi emphasised, they entail, first and foremost, massive investment – in the region of 1,200€ billion per year – as well as structural reforms and a collective capacity to act more swiftly. Against a backdrop of constrained public finances, two main levers appear to be crucial for aligning ambitions with resources: on the one hand, deepening internal integration by establishing a genuine Savings and Investment Union (SIU) ; and on the other hand, enhancing our external competitiveness by strengthening the euro’s international role.

- Furthering internal integration by establishing a genuine SIU

I shall begin with the well-known findings of the Draghi and Letta reports : for the past 25 years, Europe has been falling further and further behind the United States in terms of economic dynamism. Between 2000 and 2025, the cumulative increase in GDP per capita reached 40 per cent in the United States, compared with just 25 per cent in the eurozone. This European lag is largely due to agap in investment in research and development (R&D), which is estimated to amount to around 250$ billion each year.

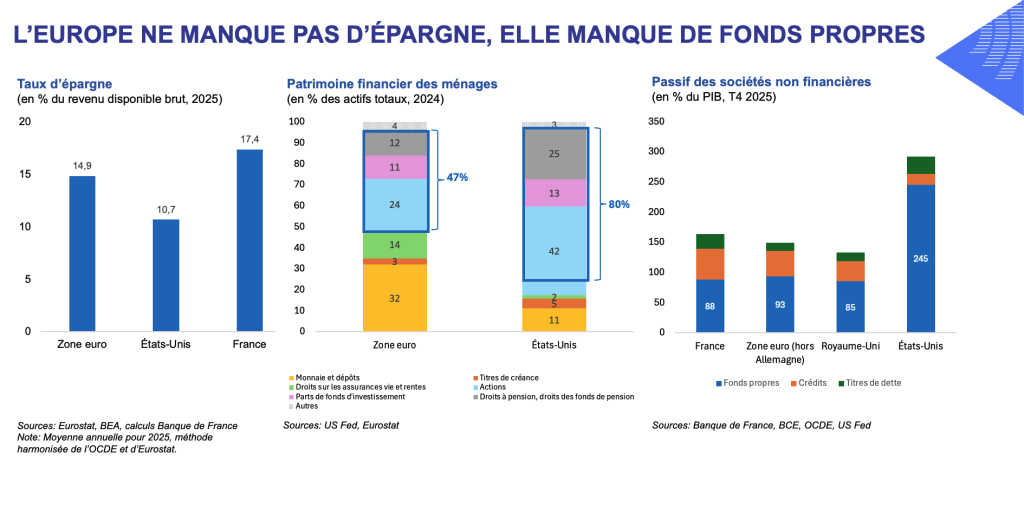

Yet the eurozone is not short of savings. The household savings rate there is higher than in the United States : 14.9 per cent of gross disposable income in 2025, compared with 10.7 per cent across the Atlantic.

The problem lies rather in the fact that savings are predominantly allocated to low-risk assets, and to a much lesser extent to investments in shares or investment funds. Europe therefore has abundant savings, but lacks equity capital, which is nevertheless essential for financing innovative companies with high growth potential. Equity financing for non-financial corporations (NFCs) thusaccounts for only 93 per cent of GDP in the eurozone, compared with 245 per cent in the United States.

This European paradox highlights the need to build a genuine Savings and Investment Union (SIU), combining the objectives of the Capital Markets Union and the Banking Union. The aim is to better reallocate Europeans’ savings to support innovative investment, particularly in three major “verticals” : AI, decarbonised energy and defence.

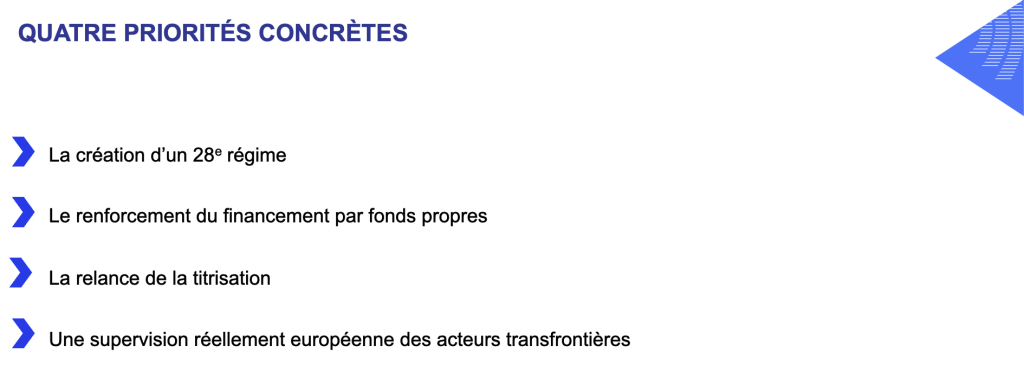

To make tangible progress, we must focus on four priorities :

- The creation of a 28th regime, in order to reduce administrative costs for European businesses, in particular the “cost of failure” ;

- Strengthening equity financing, which involves the gradual development of European retirement and pension savings schemes, the promotion of ambitious public-private partnerships in the field of venture capital, and the launch of savings products accessible to households to encourage a more diversified allocation of assets ;

- The revival of securitisation, within a transparent and secure framework, in order to increase the banking sector’s financing capacity ;

- Genuinely European supervision of cross-border players that have become systemically important, including certain market infrastructures (clearing houses, central securities depositories).

Furthermore, despite significant progress, our Banking Union remains incomplete. Its further development now calls for asimplification of the regulatory and supervisory framework. In particular, the granting of cross-border exemptions regarding capital and liquidity requirements could facilitate the integration of European banking groups, enabling them to finance our ambitions more effectively.

The establishment of a genuine EUI therefore constitutes a first lever – deepening internal integration – to align the EU’s ambitions with its resources. I now turn to a second, complementary lever, which relies on enhancing our external attractiveness by strengthening the international role of the euro. This would enable us to gain international influence, whilst reaping several concrete benefits: lower financing costs, advantages linked to invoicing trade in our own currency, and reduced dependence on the US dollar.

- Enhancing external appeal by strengthening the euro’s international role

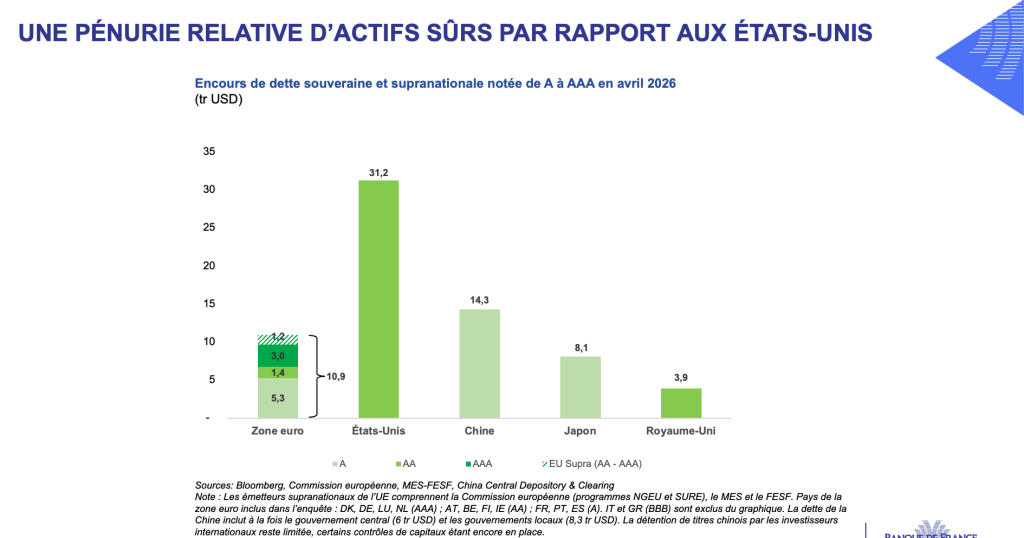

One key driver of the euro’s international role is to increase the supply of safe European assets. Even when European supranational debt is combined with eurozone sovereign bonds rated at least A, the European supply of safe assets currently stands at only 11,000$ billion – barely more than a third of US Treasury bonds.

How, then, can we increase the volume of safe assets denominated in euros ?

A first step would be to create a genuine European Treasury : we currently issue European debt under at least four different issuers – the Commission, the EIB, the ESM and the NGEU. These debts are not fungible and do not allow for the creation of a liquid market for supranational debt.

Beyond that, three options can be considered to increase the amount of safe European assets. The first would involve mergingexisting supranational debt. The second would aim to convert part of the existing sovereign debt into supranational debt through financial engineering. Finally, a third option, which we favour, would be to build on existing EU frameworks and strengthen them byfinancing joint projects through shared debt. This approach would not be based on pooling the existing debt stock, but on financingnew projects of European interest, such as the Next Generation EU programme, for example in the fields of defence, quantumtechnologies or AI.

Beyond the development of safe European assets, three further avenues can be explored. Firstly, we must further promote invoicingin euros within international value chains, where the US dollar remains predominant. Around 60 per cent of global exports are invoiced in US dollars, compared with less than 25 per cent in euros. Although the choice of invoicing currency is largely a matter for private decision-making and reflects a persistent trend, we could highlight the size of the European market, particularly in terms of investment and public procurement (SAFE, NGEU)i, to encourage invoicing in euros for these transactions.

The internationalisation of the euro must also be underpinned by a solid and robust monetary safety net. The Governing Council hastherefore recently stepped up its provision of euro liquidity lines to central banks outside the euro area (EUREP), which, combinedwith the deepening of the EUI, helps to make it more attractive for banks and businesses to finance and invoice their commercialactivities in euros.

Finally, the euro’s international standing depends on our ability to preserve the central bank currency’s pivotal role in the digital world. However, the rapid growth of dollar-denominated stablecoins held outside the United States poses the risk of the currency’s privatisation and ‘de-Europeanisation’. To address this, the Eurosystem has taken steps to offer a digital euro to the general public and a wholesale central bank digital currency (CBDC) for the interbank market. However, there is also a need for a tokenised commercial currency, whether in the form of tokenised bank deposits or euro-backed stablecoins. The challenge is clear: to adapt ourtwo-tier monetary system coherently to the tokenisation revolution, whilst fully safeguarding our monetary sovereignty.

Building European economic and monetary sovereignty therefore requires progress on two complementary fronts: greater internalintegration and greater attractiveness to the outside world. The “Delors method” – characterised by ambition, clear deadlines and collective mobilisation – can serve as our compass to achieve this. Setting a deadline for success, as my predecessor proposed, would, in this regard, be an effective way of mobilising all stakeholders. I leave you with these words of hope from Jacques Delors: “Come on, take heart, the springtime of Europe still lies ahead of us”. Thank you for your attention.

Authors

- Emmanuel Moulin Governor of the Banque de France