Blog post

A looming war for minerals?

Recommended citation

Fabry E. 2023. “A looming war for minerals?“, Blogpost, Paris: Jacques Delors Institute, 21 april.

The accelerating pace of decarbonisation around the world is fuelling a heated race for critical minerals. Countries are looking to ensure access to specific components needed to produce green technologies, as the reserves and refining capacity for these components are concentrated in just a few countries. But the risk of an escalation in export restrictions is already giving cause for concern that a conflict could erupt among countries competing for access to minerals. This will be a crucial issue in the economic security strategy being developed by the European Commission.

European countries, like China and now the United States, have chosen to provide unprecedented amounts of state aid to support the mass production of green technologies. Europe has learned its lesson from its historical dependence on Russian fossil fuels and the enduring impact it had on the competitiveness of its companies. The objective of achieving carbon neutrality by 2050 should not be accomplished by becoming even more reliant on imports of Chinese green technologies, which already hold dominant market positions, such as in the case of solar panels. Europe must develop its own production capacity to ensure national supplies and compete in the rapidly expanding global market for green tech. However, the use of export restrictions as weapons of economic coercion in the Sino-American trade war exposes Europe to the risk of disruptions in the supply of critical components.

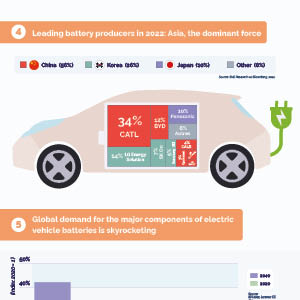

In 2020, China took the lead among the group of six countries that have placed the most restrictions on mineral exports (China, India, Argentina, Russia, Vietnam, and Kazakhstan). China’s mineral export restrictions are now nine times as great as they were in 2009[1]. On October 7, 2022, Washington decided to cut off China’s access to American technological know-how to produce advanced semiconductors. Beijing responded in January with its own plan of export restrictions, announcing that Chinese manufacturers would now need to apply for licenses if they want to export solar panel wafers and the polysilicon needed to make them. According to the International Energy Agency (IEA), China controlled 79% of global polysilicon production capacity in 2021 and 97% of global capacity for wafers. In March, it was the turn of Dutch company ASML and Japan to tighten exports of semiconductors to China, bowing to pressure from Washington. In early April, the spotlight shifted to the possibility that China may ban exports of technology to process and refine rare-earth metals. China commands 90% of the world’s rare earth refining capacity[2]. China is also weighing restrictions on exports of alloy tech for making high-performance magnets derived from rare earths. These magnets are critical components in wind turbines and electric vehicle (EV) batteries.

The importance of this new economic security issue can be illustrated using the example of access to critical minerals (lithium, cobalt, nickel, graphite) needed to produce an electric vehicle (EV) lithium-ion battery[3].

The EV market is booming, particularly in the European Union, where the IEA projects it to grow from 1.4 million vehicles in 2020 to 13.3 million vehicles in 2030, compared to 1.3 to 12 million in China and 0.3 to 8 million in the United States (India and Japan are expected to reach 3.7 million and 2.7 million vehicles respectively in 2030).

But it’s the Chinese EV makers who are seeing the strongest growth and now hold a significant share of the global market. In just one year, between 2021 and 2022, the leading Chinese manufacturer, BYD, doubled its market share from 9.1% to 18%. And when considering joint ventures like SAIC-GM-Wuling and Geely-Volvo, Chinese EV makers made up 31.6% of the global EV market in 2022. Tesla (US), Volkswagen (Germany) and Stellantis (France-Italy-US) only accounted for 13%, 8.2% and 4.7%, respectively.

This has already fuelled an increase in EU imports of Chinese EVs, which rose by a factor of 8.6 between 2020 and 2022 (reaching 6,855 vehicles). European exports to China only increased by a factor of 2.9 (reaching 1,337 vehicles). There is a similar trend in battery production. The largest Chinese manufacturers already hold 56% of the world market compared to 26% and 10% for Korean and Japanese manufacturers.

Ensuring access to the critical minerals used in lithium-ion batteries is becoming all the more urgent because global demand for these minerals – which are used in many technologies – is expected to triple on average between 2020 and 2040. European demand for lithium alone is expected to increase by a factor of 12 by 2030, presaging strong global competition for lithium resources.

In addition, countries are heavily reliant on China for the refining of these minerals, with their share of global refining capacity ranging from nearly 40% for nickel to almost 70% for graphite.

The urgency associated with this dependence on China is reflected in the target set by the European Commission in the Net-Zero Industry Act announced in March. The objective is to achieve a European production capacity, by 2030, that can cover 40% of the European Union’s demand for green technologies. The Critical Raw Materials Act presented simultaneously provides further details on the objectives for 2030. For the 34 minerals identified as critical in 2023, the objectives include: 1) intra-European extraction of at least 10% of annual EU consumption, 2) intra-European transformation of at least 40% of annual EU consumption, 3) production by recycling of at least 15% of annual consumption, and 4) not more than 65% of the EU’s annual consumption of each mineral imported from a single third country.

Extracting critical minerals in Europe will require investing more political capital to improve the social acceptability of extraction projects, as well as cutting the red tape required to obtain a permit (which takes 8 years on average). Significant investments will also be needed to diversify the EU’s sources of critical minerals, which will play a decisive role in meeting European supply requirements. Taking lithium for example, the EU depends on Australia for 87% of its supply of raw lithium, and on Chile for 78% of its supply of refined lithium (two countries that have become highly coveted for their mineral reserves). The EU started by signing a strategic partnership on raw materials with Canada in 2021. Concluding the trade agreement currently being negotiated with Australia and ratifying the one signed with Chile in 2022 also carries strategic significance for the EU given that these two deals aim to guarantee fair and equal access for European companies to the mineral exports of these two countries. The EU should also pursue more ad hoc agreements, such as those signed in 2022 with Kazakhstan and Namibia for hydrogen production and access to critical minerals. Even the agreement signed with Mercosur in 2019, which has not yet been ratified, takes on greater significance when considering the mineral reserves of the trade bloc’s members. Brazil is home to the world’s third-largest reserves of nickel and graphite. Argentina has the second-largest reserves of lithium in the world. And so on.

But the road is long. Not only does China, on its own, account for nearly 65% of the world’s lithium refining capacity, but the country is signing contract after contract for lithium extraction in countries such as Chile, Argentina, and Zimbabwe. China also has control of 90% of the world’s refining capacity for rare earth minerals and over 70% for cobalt. Europe must regain the refining capacity it possessed in the 1990s for rare earths and other minerals, similar to the United States and Japan, which also outsourced this expertise and production to China. This will require significant investment in greening technologies to ensure that the installation of new infrastructure is socially acceptable. It also means investing in the development of technological alternatives such as sodium-ion batteries.

On March 30, the President of the European Commission, Ursula von der Leyen, emphasised that the priority for Europe is not to align with the US strategy of decoupling but to reduce the risks associated with excessive reliance on China. Xi Jinping nevertheless has a formidable weapon of retaliation against any country or company he wishes to target. While Europe can still benefit from China’s dependence on the European single market, Beijing is on the hunt for new commercial relationships with southern countries. The recalibration of Europe’s strategy towards China will thus be a key driving principle of Europe’s forthcoming economic security strategy.

Notes

[1] “Raw materials critical for the green transition. Production, international trade and export restrictions”, Przemyslaw Kowalski and Clarisse Legendre, OECD, April 11, 2023.

[2] “China weighs export ban for rare-earth magnet tech”, Shunsuke Tabeta, Nikkei Asia, April 6, 2023.

[3] “Achieving net zero while lessening reliance on China: The example of minerals used in electric vehicle batteries”, Infographics, Elvire Fabry, Sacha Courtial et Renato Farfoglia, Institut Jacques Delors, March 13, 2023. Most of the data sources cited in this article are derived from this infographic.

SUR LE MÊME THÈME

ON THE SAME THEME

PUBLICATIONS

Invest in Europe First!

Taiwan and European strategic autonomy

Achieving net zero while lessening reliance on China

Europe’s response to the Sino-American rivalry

Building the strategic autonomy of Europe while global decoupling trends accelerate

Reducing the EU’s dependence on chinese imports of rare earths and other strategic minerals

European companies are facing the decoupling of China and the United States

LEVERAGING TRADE POLICY FOR THE EU’S STRATEGIC AUTONOMY

Strategic Autonomy

in Post-Covid Trade Policy

European Strategic Autonomy

and the US–China Rivalry:

Reducing the EU’s strategic dependence

MÉDIAS

MEDIAS

Comment l’Espagne est devenu le nouvel eldorado de la Chine

La lente marche des Vingt-Sept vers l’autonomie stratégique européenne

Renault boss: War of the future will be over critical raw materials